2026 Real Estate Market Trends: What Buyers and Sellers Need to Know

Apr 01, 2026

Written by David Dodge

After years of sky-high mortgage rates, razor-thin inventory, and frustrated buyers, the U.S. real estate market is slowly—but surely—shifting. This month, we break down what's actually happening, what the data says, and what it means for you, whether you're a first-time buyer, a curious renter, or someone who simply wants to understand the news.

No jargon, no filler. Just the essential facts, explained from scratch.

01. First Things First: What Is the "Housing Market," Anyway?

If you've ever heard a news anchor say "the housing market is cooling" and wondered what that actually means, you're not alone. The term can feel abstract—but it's actually pretty straightforward once you know the basics.

📖 Quick Definition

The housing market refers to the buying, selling, and renting of homes across the country (or in a specific area). Just like a stock market tracks the prices of company shares, the housing market tracks home prices, the number of homes available for sale (called inventory), how fast homes sell, and the cost to borrow money to buy one (called the mortgage rate).

When people say the market is "hot," they mean homes are selling fast, often above asking price, and buyers are competing aggressively. When it's "cooling," homes sit longer, prices soften, and buyers have more negotiating power. Right now, in April 2026, the market is in a fascinating middle state—and understanding it can genuinely save you money or help you make a smarter life decision.

6.38%

30-yr Fixed Mortgage Rate

(Mar 26, 2026 — Freddie Mac)

$398K

Median Home Price

(Feb 2026 — NAR)

4.09M

Existing Home Sales

(Feb 2026 — NAR)

3.8 mo

Months of Housing Supply

(Feb 2026 — NAR)

02. Mortgage Rates: The Number That Changes Everything

If there's one number that shapes the entire housing market more than any other, it's the mortgage rate. Here's why it matters so much: Most people don't pay for a home in cash. They take out a mortgage—essentially a loan from a bank—and pay it back over 15 or 30 years. The mortgage rate determines how much interest you pay on top of the actual price of the home. Even a 1% change in the rate can add or remove hundreds of dollars from your monthly payment.

To put this in perspective: back in early 2021, mortgage rates hit a record low of just 2.65%. A $400,000 home loan at that rate would cost roughly $1,619 per month (principal + interest). Today, with rates around 6.38%, that same loan costs about $2,500 per month—that's nearly $900 more every single month.

The good news? Rates are coming down from their 2023 peak near 8%. According to Freddie Mac, the 30-year fixed rate stood at 6.38% as of March 26, 2026—still elevated, but meaningfully lower than a year ago when it averaged 6.65%. And forecasters see further relief ahead.

Fannie Mae's latest forecast (March 2026) projects rates dipping to 5.9% in Q2 2026, 5.8% in Q3, and 5.7% by year-end—the first time they'd fall below 6% since 2022. These projections are more optimistic than the previous month's forecast, driven largely by signs of slower economic growth and expectations for further Federal Reserve action.

"Monthly payments are expected to ease for the first time since 2020—mortgage rates coming down, combined with rising incomes, means affordability is genuinely improving."

— NAR Housing Economists, 2026 Outlook

03. Home Prices: Still High, But Growth Is Stalling

Here's a number that might surprise you: the median existing home sold in the U.S. in February 2026 cost $398,000. That's according to the National Association of Realtors (NAR)—the industry's main tracking body. For context, the same number back in 2019 was around $272,000. Prices have climbed roughly 46% in about six years.

But the rate of increase is slowing down sharply. Different forecasters see different outcomes depending on the region:

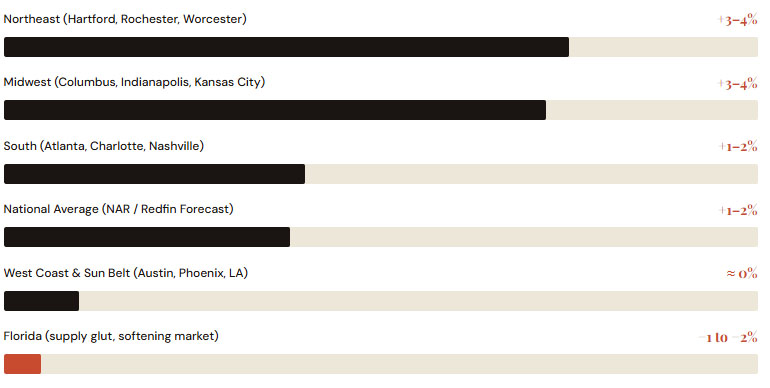

Projected Home Price Growth by Region — 2026

Estimated year-over-year % change; national forecasts range from 0–4%

Sources: Axios / Redfin / Cotality · J.P. Morgan Global Research · NAR Economists

Why such a big difference between regions? It comes down to supply and demand—the most basic economic concept there is. In the Northeast and Midwest, there simply aren't enough homes being built to keep up with the number of people who want to live there. That scarcity keeps prices rising. In contrast, Florida and parts of Texas saw a construction boom during the pandemic, and that extra supply is now putting downward pressure on prices.

J.P. Morgan's research team projects that home prices will essentially stall at 0% nationally in 2026—though as we can see from the chart, that national average hides a lot of regional variation. If you live in Connecticut, your home may grow in value meaningfully. If you're in Austin or Miami, prices could be flat or slightly negative.

04. Inventory: More Homes for Sale — But Still Not Enough

One of the most discussed topics in real estate right now is inventory—that is, how many homes are currently available for people to buy. For most of 2022 through 2024, inventory was historically low. Many homeowners who locked in ultra-low mortgage rates in 2020–2021 refused to sell, because doing so would mean giving up their cheap loan and taking on a new one at 7%+. Economists called this the "lock-in effect."

📖 The "Lock-In Effect" Explained

Imagine you bought a home in 2021 at a 3% mortgage rate. Your monthly payment is very affordable. If you sell and buy a new home today at 6.38%, your payment nearly doubles—even if the new home costs the same. So you stay put. Multiply this by millions of homeowners, and you get a massive shortage of homes for sale. This is the lock-in effect, and it's been a key reason the market has been so competitive for buyers.

The good news: the grip of the lock-in effect is loosening. NAR's data shows inventory levels are about 20% above those of one year ago, giving buyers meaningfully more choices than in 2024. February 2026 saw 3.8 months of housing supply—a measure of how long it would take to sell every home on the market at the current pace. (A balanced market is typically around 5–6 months.)

Still, we're not back to normal. Pre-pandemic inventory levels remain out of reach in most markets, and economists at NAR are clear that the only real long-term fix is to build more homes. This challenge runs into zoning laws, construction costs, and labor shortages. The National Association of Home Builders expects 1.05 million new homes to be built in 2026, up 4% from 2025.

| Region | Inventory Trend | Price Outlook | Market Type |

|---|---|---|---|

| Northeast | Still Below Pre-Pandemic | +3–4% | Seller's Market |

| Midwest | Recovering Slowly | +3–4% | Seller's Market |

| South | Improving / Near-Balanced | +1–2% | Balanced |

| West Coast | Supply Glut in Some Areas | ≈0% | Buyer-Leaning |

| Florida / Sun Belt | Elevated Supply | −1 to −2% | Buyer's Market |

05. Who's Buying? Market Sentiment Is Picking Up

Beyond the cold numbers, there's a human element to the housing market that matters just as much: how are people actually feeling about buying right now? After a few years of deep frustration—buyers losing bidding wars, being priced out, or simply giving up—the mood is noticeably shifting.

According to a recent industry report citing NAR data, real estate agents' confidence in buyer traffic has jumped from 27% to 37% year-over-year. Showings are up. Offers are more frequent. Spring 2026 feels more energetic than any spring in the past three years.

Interestingly, NAR economists are also tracking a fascinating demographic shift: single women are becoming one of the fastest-growing segments of homebuyers. This reflects broader social trends, including lower marriage rates and a generation of women building independent financial wealth. First-time buyers, meanwhile, are finally seeing a bit more breathing room thanks to the conventional loan limit rising to $832,750—meaning more people can access financing for higher-cost homes with as little as 3% down.

The rental market is also showing interesting dynamics. With homeownership still stretched on affordability, many people are choosing to rent for longer—especially Gen Z entering the workforce. Redfin projects rental prices will rise 2–3% by the end of 2026, with single-family rentals (SFRs) emerging as one of the hottest investment categories.

🏠 Practical Tips for First-Time Buyers in 2026

- Get pre-approved before you shop. In a competitive market, a pre-approval letter shows sellers you're serious and can move fast. It also tells you exactly what you can afford so you don't fall in love with a home out of your range.

- Don't wait for "perfect" rates. Rates may continue falling slowly, but they could also tick back up. If you find a home you love and can afford the payment, waiting for a better rate might cost you the house. You can always refinance later if rates drop significantly.

- Look at the Midwest and affordable metros. Cities like Columbus, Indianapolis, and Kansas City offer strong job markets, good quality of life, and home prices that are far more accessible than coastal cities. These markets are expected to see solid appreciation in 2026.

- Mid-April is statistically a great time to buy. NAR's data shows the week of April 12–18 historically sees the best combination of active listings, competitive prices, and strong buyer demand. You face competition, but also the widest selection.

- Explore adjustable-rate mortgages (ARMs). If rates are expected to fall, an ARM—which starts lower and adjusts after 5 or 7 years—might cost you less in the near term. Just make sure you understand the risks if rates don't fall as predicted.

06. Beyond Houses: What's Happening in Commercial Real Estate?

Real estate isn't just homes. Commercial real estate (CRE) covers office buildings, shopping centers, warehouses, apartment complexes, and more. And in 2026, the commercial side of the market is showing some of the most dramatic divergence we've seen in decades.

CBRE's 2026 U.S. Real Estate Market Outlook projects commercial real estate investment will jump 16% this year to $562 billion—nearly matching pre-pandemic averages. That's a strong signal that institutional money (think pension funds, REITs, and large investment firms) is flowing back into the market.

But not all sectors are equal. The big divide is in office space. The rise of remote and hybrid work hasn't fully reversed, meaning older office buildings are struggling with vacancies. However, brand-new, premium ("Class A") office spaces in prime locations are seeing a scarcity of available supply—companies that do require in-person work are competing for the best buildings. Expect even more scarcity of available prime office space by year-end 2026, according to CBRE.

The real winner in commercial real estate? Data centers. Fueled by the explosion in artificial intelligence infrastructure, demand for purpose-built data facilities is soaring. This is perhaps the hottest sub-sector in all of real estate right now, attracting billions in investment from both tech giants and real estate investors.

07. The Big Picture: Is 2026 a Good Time to Buy?

This is the question everyone wants answered. The honest answer: it depends on your situation—but the conditions are genuinely better than they've been in several years.

Here's how to think about it. The Compass 2026 Housing Market Outlook frames this year as a transition from the extreme post-pandemic disruption toward something more "normal." The unusual dynamics of 2020–2024—frozen inventory, frenzied bidding wars, pandemic-driven migration—are fading. In their place, a more rational, data-driven market is emerging.

For buyers: You have more choices than a year ago, rates are trending down, and seller negotiating power is weakening in many markets. If affordability works for your budget—and you're planning to stay put for at least 5 years—2026 can be a good time to enter the market. Don't try to time the absolute bottom; focus on what makes sense for your life.

For sellers: The market still leans in your favor in most parts of the country, particularly the Northeast and Midwest. Spring is the prime selling season, and data shows mid-April is historically one of the strongest weeks of the year. List your home well, price it fairly based on recent comparables, and you'll likely do well.

For investors: The single-family rental market remains compelling, especially in supply-constrained suburban markets. Data centers and industrial/logistics properties are also strong bets for institutional money. Office is risky unless you're targeting the premium end of the market. Multifamily remains solid in cities with strong job growth.

One key risk to watch: geopolitical uncertainty. Recent events have caused some volatility in mortgage rates, and a broader economic slowdown could dampen job growth and buyer demand. The housing market doesn't exist in a bubble—what happens to the broader economy matters enormously.

|

Term |

Definition |

|---|---|

|

Mortgage Rate |

The interest rate charged on a home loan. Higher rates = bigger monthly payments for the same-priced home. |

|

Inventory |

The number of homes currently for sale. Low inventory = more competition among buyers and higher prices. |

|

Median Home Price |

The median price of all homes sold—half sold for more, half sold for less. More reliable than "average." |

|

Months of Supply |

How long would it take to sell all current listings at the current sales pace? Under 3 = very tight; 5–6 = balanced. |

|

Lock-In Effect |

When homeowners refuse to sell because they don't want to give up their low existing mortgage rate. |

|

ARM (Adjustable-Rate Mortgage) |

A mortgage with a fixed rate for a few years, then adjusts periodically. Often starts lower than fixed-rate loans. |

|

Pre-Approval |

A lender's conditional commitment to loan you up to a certain amount. Makes you a more competitive buyer. |

|

Cap Rate |

A measure of return on a real estate investment, calculated as net income divided by property price. |