2026 US Housing Market: Capitalizing on Refuge Markets

May 22, 2026

Written by David Dodge

The geographic split in today's housing market is one of the sharpest we've seen in a generation. Here's how to coach your clients out of overheated dead ends and into places where smart offers still win.

Let me be blunt with you. If you are still sending buyers to Austin, Tampa, or Phoenix the same way you were two years ago — running the same comp analysis, writing the same offer letters, telling them to expect competition — you are doing them a disservice. The map has flipped, and a lot of agents haven't caught up to it yet.

We are in the middle of a genuine geographic polarization in U.S. real estate, and the gap is widening by the month. On one side you have Sun Belt and West Coast markets drowning in inventory, where sellers are chasing buyers with price cuts. On the other side you have a cluster of secondary Northeast and Midwest cities — I call them "refuge markets" — where inventory is historically scarce, competition is brutal, and buyers who show up prepared are building equity the day they close.

Understanding this split, and knowing how to explain it to clients, is one of the most valuable tools in your kit right now. This is the framework I've been using.

The Split Is Real — and It's Getting Wider

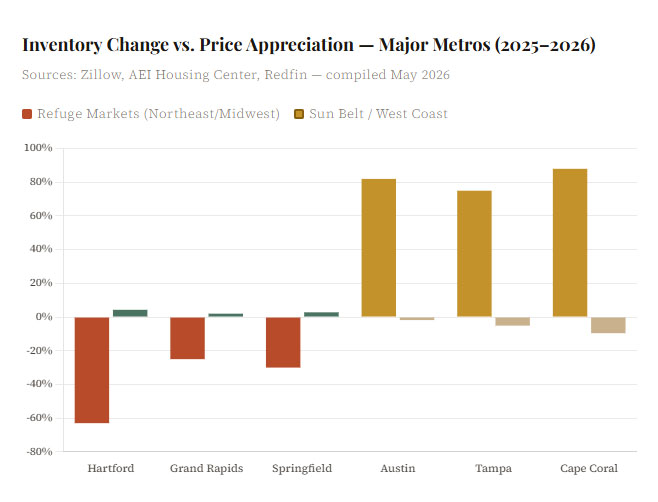

Here is the core data point you need to internalize: 28 out of America's 53 largest metros saw year-over-year price decreases through February 2026, and virtually every one of them is in Florida, California, or Texas. At the same time, cities like Kansas City, Pittsburgh, and Cleveland — places people were sleeping on for decades — are posting gains between 5 and 9 percent over the same period. That is not a minor divergence. That is a structural reshaping of where value lives in this country.

The cause isn't complicated. During the pandemic boom, builders went absolutely wild in the Sun Belt. Population was surging, remote workers were fleeing expensive coastal cities, and it felt like the growth would never stop. Texas added 391,243 people between July 2024 and July 2025, nearly two and a half times faster than the national average, so the building frenzy made sense at the time. But when mortgage rates climbed and remote-work flexibility started shrinking — remote job postings dropped from a pandemic peak of roughly 20% of all listings to around 7–8% by 2026 — that demand evaporated faster than the inventory could be absorbed. Now you have oversupply chasing diminishing demand in exactly the markets that got overbuilt.

“You could almost cut and paste the ‘best’ performers from February 2022 into the current ‘worst’ column, and vice versa.”

— Fortune, citing AEI Housing Center data, April 2026

Welcome to the Refuge Markets

So where should your buyers be looking? The cities I keep coming back to are the ones that never got overbuilt in the first place — and where the fundamental case for buying has only gotten stronger as the Sun Belt has softened.

Hartford, Connecticut: The #1 hottest market in the country

Zillow's 2026 hottest markets rankings moved Hartford to the top spot, and when you look at the numbers, it's not even close. Inventory is 63% below pre-pandemic levels — the largest deficit among the 50 largest U.S. metros — and more than two-thirds of Hartford homes sold above asking price in 2025. Zillow forecasts continued value growth near 4% for 2026 following a 4.3% gain the year before. This is not a market where buyers browse leisurely. You show up prepared and you move fast, or someone else gets the house.

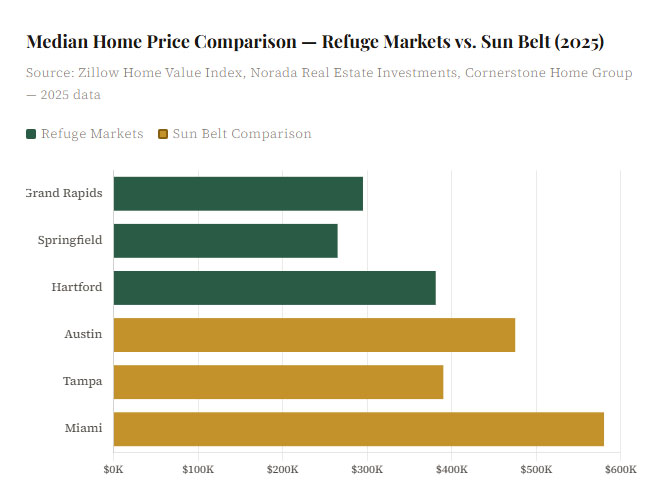

The play for your clients? Hartford is the value proposition that Boston and New York can't offer anymore. Hartford's typical home value sat at roughly $381,760 in late 2025 — a fraction of what comparable square footage costs 90 minutes south in metro Boston. For remote workers with a hybrid schedule who need New York or Boston accessibility a few times a week, it's a no-brainer budget unlock.

Springfield, Massachusetts and the Pioneer Valley

The whole Connecticut River Valley corridor — from Hartford up through Springfield and into the Pioneer Valley — is operating under the same supply pressure. These markets have benefited from the same affordability migration patterns as Hartford without receiving as much national attention. That relative obscurity is exactly what makes them interesting for agents with out-of-state clients.

A buyer who can't touch a reasonable single-family home in suburban Boston can often find twice the square footage in Springfield for the same money. Factor in access to Amtrak service to Boston and New York, a strong regional university presence that keeps the rental market healthy, and serious inventory constraints, and you have a setup that's hard to argue against.

Grand Rapids, Michigan: The Midwest sleeper

Grand Rapids keeps showing up in every serious competitive market analysis, and for good reason. Available housing stock in Grand Rapids sat at roughly 573 units listed for sale as of September 2025, creating intense competition and explaining why well-priced homes often receive multiple offers within days of listing. The inventory shortage comes largely from the lock-in effect — homeowners holding 2–3% mortgages aren't moving unless they have to, which keeps resale supply pinched.

Median home prices in Grand Rapids reached approximately $293,000 to $298,000 in late 2025, with year-over-year appreciation around 1.6% to 2.1%. For buyers comparing that against Miami at $400,000+ with negative appreciation, or Austin where prices are actively declining, the math is straightforward.

Beyond just the price point, Grand Rapids has a genuinely diversified economy built around healthcare, manufacturing, and a growing technology sector — which is exactly the kind of demand base that supports long-term housing value without requiring hot speculative money to keep things afloat.

The 45-Minute Radius Framework

Here's the coaching piece that I've found makes the biggest difference when working with clients who are stuck in a metro-or-nothing mindset. I call it the 45-minute radius framework, and it works in almost every major Northeast and Midwest hub.

The idea is simple: take whatever major city your client is anchored to — Boston, New York, Chicago, Philadelphia — and draw a circle representing a 45-to-60 minute drive or train ride. Everything inside that radius is commutable on a hybrid schedule, which means a buyer who goes into the office two or three days a week doesn't actually need to live in or adjacent to the city. They need to be close enough to make the trip without destroying their quality of life.

Boston → Hartford: 100 miles / ~90 min by train. Typical home price $381K vs. $717K in metro Boston. Roughly triple the square footage for the same budget.

New York → Springfield, MA: 150 miles. Expanding commuter rail access. Home prices under $270K vs. $900K+ in metro NYC.

Chicago → Grand Rapids: 180 miles / ~2.5 hrs. Viable for weekly or biweekly commutes. Home prices under $300K vs. $450K+ in suburban Chicago.

Philadelphia → Allentown / Bethlehem: 60 miles / under an hour. A growing refuge corridor for remote-partial workers seeking affordability.

The key mental shift you're coaching your client through is that commutable no longer means daily. For hybrid workers, the relevant question isn't "can I do this every morning?" It's "can I do this Tuesday and Thursday without losing my mind?" That's a very different distance calculation, and it opens up a completely different set of markets.

The Negotiation Window Is Genuinely Different

I want to spend a minute on something that doesn't get talked about enough in these market comparison conversations, which is the psychological and practical difference in how offers work in these two environments.

In an overbuilt Sun Belt market right now, your buyer walks in with leverage. In Austin, Texas, sellers outnumber buyers by more than 2:1, and San Antonio is similar — this is the widest seller-buyer ratio gap in over a decade. Sellers are cutting prices, offering concessions, and accepting contingencies. Your client can take their time, get proper inspections, and negotiate repairs. That is nothing.

But here's what I keep telling my agents: that negotiating leverage in a declining or stagnant market is only valuable if the underlying asset is going to hold its value. If you're getting a great deal on something that's going to be worth less in two years, was it actually a great deal? The leverage in a refuge market works differently — you're competing harder upfront, but you're competing for an asset that has a structural inventory shortage behind it and a decade-long track record of quiet, steady appreciation.

“Competition among buyers will be stiff, and sellers will have the upper hand in this year's hottest markets.”

— Zillow 2026 Housing Forecast

Coaching the Out-of-State and Remote-Work Buyer

The client profile that benefits most from this conversation is the out-of-state or remote-partial buyer — someone currently in a high-cost market, watching their equity potential flatten, who has flexibility in where they live but hasn't fully thought through what that flexibility is actually worth in dollar terms.

Here's the coaching script I use. I ask three questions. First: how many days a week do you actually need to be physically present? Not how many days you prefer, not how many days your current commute assumes — how many days is genuinely required. Second: what's your real budget constraint, and are you current on what that budget actually buys in the markets you're considering? Third: if you could buy a home that's likely to appreciate 4% a year in a market where you could get three times the space, how long would the longer commute have to be before it stopped making sense?

That third question is the one that usually shifts the conversation. When you put actual numbers on the buying power differential — and it is frequently a $200,000 to $300,000 swing in what the same budget buys — the calculus changes fast.

1. Anchor the commute reality

Get the exact number of required in-office days per week in writing. Everything else flows from this.

2. Run the budget spreadsheet

Show side-by-side what $400K buys in the metro core vs. 45–60 minutes out. Let the square footage and condition do the talking.

3. Model appreciation vs. commute cost

A 3–4% annual appreciation differential on a $380K home compounds to real money over five years. Put that number next to annual transport costs.

4. Prequalify for the speed required

Refuge markets move in days, not weeks. Pre-approval, financial docs, and offer strategy need to be ready before you see the first house.

What This Means for Your Business

There is a practical business angle here that I don't want to gloss over. Agents who specialize in cross-metro relocation and secondary market expertise are genuinely differentiated right now. The information asymmetry between what a client who's been searching in Austin for six months knows and what an agent who's been tracking Hartford and Grand Rapids knows is enormous — and it's the kind of gap that earns referrals.

Buyers have been trading big-city job hubs for cheaper metros and rural communities, often armed with remote-work incomes — and a lot of them are doing it with incomplete information about which markets are actually positioned to reward that move. Being the agent who has already studied these markets, who knows the commute options, and who can show up with a ready-to-go offer strategy is a differentiating position that most of your competitors haven't claimed yet.

The geographic polarization isn't going to resolve quickly. Sun Belt oversupply takes years to absorb, and Northeast/Midwest inventory constraints are structural — they're not going to be solved by a six-month building surge. If anything, the divide is likely to get wider before it gets narrower.

The agents who do the work to understand this now, who build the client coaching language around it, who get familiar with what $380,000 actually buys in Hartford or Grand Rapids, are the ones who are going to be well-positioned when the next wave of hybrid workers starts looking for a smarter way to deploy their budgets. That wave is already here. The question is whether you're ready for it.

</p

</p