Buy a Home in St. Louis Without Getting Outbid (2026)

May 29, 2026

Written by David Dodge

A first-timer's field guide to the 2026 spring market — the neighborhoods, the numbers, and the moves that actually win deals.

Let me tell you what nobody warns you about when you start shopping for a home in St. Louis. It's not the mortgage rate — you've probably already stressed about that. It's not even saving for a down payment, though that deserves its own conversation. The thing that actually blindsides most first-time buyers is the geography problem: this market does not behave like a single market.

If you walk into St. Charles County, with the same patience you'd bring to St. Louis City, you will lose every home you try to buy. And if you walk into St. Louis City ready to waive every contingency and overbid by 5%, you'll probably overpay for something you didn't need to fight for. The two markets are running on completely different clocks — and if you don't know which clock you're on, you're already behind.

This guide is built around what the 2026 spring data is actually showing. Not generic homebuying advice. Not a repackaged national trend piece. This is specific to the St. Louis metro — the neighborhoods, the programs, the offer strategies — and I'm going to walk you through it the way I'd walk a client through it.

Phase 1 — Location Strategy

Stop Treating St. Louis Like One Market

Here is the most important thing I can tell you about buying in the St. Louis metro in 2026: where you buy determines how you buy. The tactical moves that get you a house in Kirkwood will make you look like you don't know what you're doing in Tower Grove South. And the patience that serves you beautifully in St. Louis City will cost you every single house you try to get in St. Charles County.

So let's lay out the actual landscape before we talk strategy.

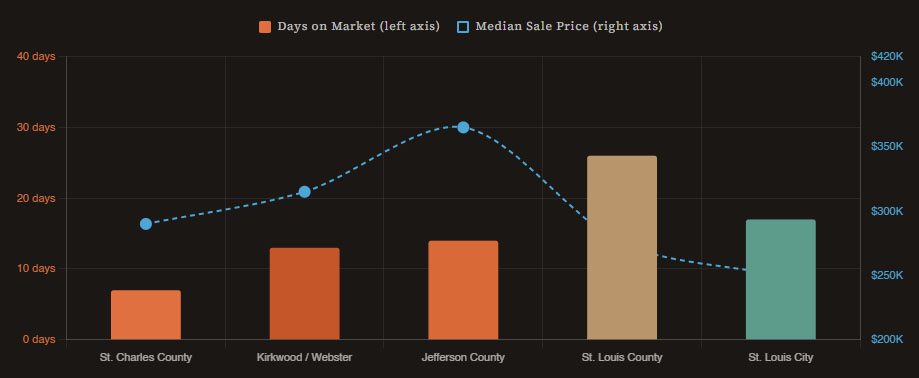

Days on Market & Median Price by Area — Spring 2026

St. Louis Metropolitan Statistical Area · April–May 2026 Data

The chart above tells the story more clearly than any paragraph can. St. Charles County is operating in a completely different reality than St. Louis City — not just in price, but in the pace at which you have to make decisions. Seven days. That's not a stat designed to pressure you. That's just how fast well-priced homes are disappearing in O'Fallon, Wentzville, and St. Peters.

Here's a breakdown of where things stand across the key submarkets as of spring 2026:

What I want first-time buyers to take from this table is not just where prices sit — it's what the supply number means for your leverage. A 1.9-month supply in St. Louis County means sellers still have the upper hand on desirable single-family homes. A 3.5-month supply in St. Louis City means you can actually have a conversation about price and concessions without immediately losing the deal.

For buyers who prioritize newer construction, school district reputation, and suburban walkability, St. Charles County is where the demand is concentrated — but you'll pay for it in speed, not just price. For buyers who want square footage per dollar and can trade some commute for space, North County communities like Florissant and Hazelwood are delivering the best value in the entire metro right now.

"In St. Charles County, a well-priced home isn't sitting. It's competing — and sellers know it. Seven days on market is not a stat, it's a strategy."

— HouseSoldEasy.com, April 2026 Market Report

What does this mean practically? If you are targeting St. Charles County or the hot pockets of St. Louis County like Kirkwood, Crestwood, or Webster Groves, you need to walk into this process already pre-approved — not pre-qualified, pre-approved — and you need to have already decided on your non-negotiables. Because when a house hits the MLS at 9 AM, and you're scheduling a showing for the weekend, it's already gone. If you are more price-sensitive or need more time to make decisions, St. Louis City is genuinely worth the look. The city's median sale price of around $224,000 to $250,000 is one of the lowest entry points in the region, and buyers there are landing deals at an average of 98.6% of list price, which means there is actually some negotiating room.

Phase 2 — Financial Prep

The Real Numbers Nobody Tells You About Until It's Too Late

I've seen buyers get fully pre-approved for a mortgage and then come up short at the closing table because nobody broke down what "cash to close" actually means in the St. Louis market. The down payment is not the only number. It's not even the biggest surprise for most buyers. Here's what you're actually writing checks for:

-

1 Earnest money deposit (1–2% of purchase price): This goes down immediately when your offer is accepted — typically within 24 to 72 hours. On a $275,000 home, that's $2,750 to $5,500 out of your bank account before anything else happens. It applies toward your down payment at closing, but you need the liquid cash before you need the loan.

-

2 Home inspection ($350–$550): Paid directly to the inspector, usually at the time of the inspection — not at closing. Do not skip this in a competitive market. I know the temptation. Don't do it. A clean inspection report is also a negotiating leverage if things come up.

-

3 Appraisal fee ($500–$700): Required by your lender, also paid out-of-pocket before closing in most cases. The appraisal determines whether the lender will actually fund the purchase at the agreed price — important in competitive markets where offer prices can exceed appraised values.

-

4 Closing costs (2–4% of the loan amount): This is the biggest surprise line item. On a $275,000 purchase with a 5% down payment, your loan is roughly $261,250 — meaning closing costs land somewhere between $5,225 and $10,450. These include lender fees, title insurance, prepaid taxes, prepaid homeowners insurance, and a dozen smaller items.

-

5. Down payment: For most first-time buyers using FHA financing, this is 3.5% of the purchase price. On a $250,000 home, that's $8,750. Conventional loans with PMI can go as low as 3–5% down. This is the number most buyers know — but it's rarely the one that catches them off guard.

Add all of this up, and a typical first-time buyer purchasing a $250,000 home in St. Louis County needs somewhere between $18,000 and $28,000 in liquid assets to close — not counting moving expenses, initial repairs, or that couch you're going to need. Most people save for the down payment and forget everything else. Don't be most people.

The good news — and this is where St. Louis genuinely has an edge over markets like Chicago, Nashville, or Denver — is that housing costs here remain approximately 21.2% below the national average. You are operating in one of the most affordable large metros in the country, which means these numbers, while real, are more manageable here than almost anywhere else.

Mortgage rates as of late April 2026 are hovering around 6.40% on a 30-year fixed loan, slightly down from the 6.57% average seen a month prior. Most economists expect rates to stay in the 6% to 6.5% range through the rest of spring, with a possible drift lower if inflation continues to ease. The message for buyers: you're unlikely to get a dramatically better rate by waiting, and every month you sit on the sideline is equity you're not building.

Phase 3 — Assistance Programs

The MHDC Programs That Can Make You Instantly Competitive

This is the section that changes the math for a lot of first-time buyers, and it's the one most people skip over because they assume they won't qualify or the programs are too complicated to bother with. Let me clear that up right now.

The Missouri Housing Development Commission — MHDC — runs the most important first-time buyer programs in the state, and if you're buying in St. Louis and you haven't looked into these, you are leaving money on the table—potentially thousands of dollars.

MHDC First Place Loan Program

Missouri's flagship first-time buyer program offers 30-year fixed-rate loans through approved lenders statewide. The program works with FHA, VA, USDA, and HFA Advantage conventional loans.

Eligible buyers may receive up to 4% of the loan amount to help cover down payment and closing costs. On a $260,000 loan, that's up to $10,400 in assistance.

The assistance is forgiven after 10 years if the home remains your primary residence. Buyers must meet income and purchase price limits, complete a homebuyer education course, and have a qualifying credit score.

There's also a non-cash assistance option for buyers who already have funds for upfront costs but want a lower interest rate. In that configuration, the program typically offers rates 0.25% to 0.50% below what you'd get through the standard DPA option, which compounds significantly over the life of a 30-year mortgage.

What makes MHDC programs especially useful in a competitive market is the pre-approval clarity they give you. When you show up at an offer table with a fully structured MHDC-backed pre-approval, you're not a buyer who might figure out financing — you're a buyer who already has. That distinction matters more than most people realize in a market where sellers are evaluating offer risk alongside offer price.

One more thing worth knowing: MHDC programs can be stacked with other local assistance programs in many cases. If you're buying in a specific city or county that has its own down payment grant or assistance program, check with a certified MHDC lender about combining them. The rules vary, but it's not uncommon for buyers to layer programs and reduce their out-of-pocket costs significantly.

Who Qualifies for MHDC Programs?

- First-Time Buyer: You cannot have owned a primary residence within the last three years. Exceptions may apply for qualified veterans and certain target areas.

- Income & Purchase Price Limits: Household income and home purchase price must fall within MHDC guidelines, which vary by county and family size.

- Credit Score: Minimum credit score requirements apply. FHA borrowers typically need a score of 580 or higher, though some lenders may require more.

- Homebuyer Education: Completion of an approved homebuyer education course is required. Most courses are available online and take approximately 6–8 hours.

Phase 4 — Winning the Offer

The 24-Hour Offer Framework for Hot Pockets

Everything up to this point has been preparation. This is where that preparation pays off — or doesn't, depending on how you approach the offer phase.

In high-velocity submarkets like Kirkwood, Webster Groves, and St. Charles County, the window between "a house went active on the MLS" and "that house already has three offers" can be less than 24 hours. I'm not exaggerating. In peak spring 2026 conditions, hot homes in desirable school districts are going under contract in 11 to 15 days in Kirkwood and Webster Groves — and that's the slow end. St. Charles County's median days on market is 7.

This means the old mental model — browse on the weekend, schedule a showing next week, think it over for a few days — is not a strategy. It's a guarantee that you'll be perpetually looking at homes someone else bought.

Here's the framework that works in these markets:

-

1 Set up real-time MLS alerts the day before you're ready to move. Not "pretty ready" — actually ready. Pre-approval in hand, budget confirmed, must-haves defined. When an alert hits your phone for a home that checks your boxes, that's not a browsing notification. That's a decision moment.

-

2 Schedule showings for the same day or the next morning, maximum. If a home goes live on a Tuesday and you wait until Saturday to see it, you've almost certainly already missed it in a hot submarket. Block time in your schedule during the active search period specifically for same-day or next-day showings.

-

3 Write clean offers with minimal contingencies — but keep your inspection. In competitive markets, sellers are comparing offers not just on price but on offer "cleanliness." An offer with five contingencies, a 45-day close, and a home-sale contingency is less attractive than a clean offer at the same price with a 30-day close and only a standard inspection contingency. Know in advance what you're willing to waive and what you're not.

-

4 Understand the list-price-to-sale-price ratio for your specific target area. In St. Louis City, buyers are averaging 98.6% of the list price — meaning there's some room. In Jefferson County and hot St. Charles pockets, buyers are paying 100–101.3% of the list price. Going in at the asking price in one area is competitive; in another, it's the floor. Your offer strategy needs to be calibrated to the specific neighborhood, not the broader city.

-

5 Write a genuine, specific escalation clause if the home is a real priority. An escalation clause says, "I'll beat any competing offer by $X up to a maximum of $Y." These work best when the home is priced correctly from the start, not when the seller is testing an aspirational price. Used correctly in the right market, they can secure a home without massively overpaying — because you're not guessing at a ceiling, you're responding to actual competition.

"Pricing right from day one is not optional anymore. In a market where months' supply is stabilizing, sellers who overprice are sitting; sellers who price correctly are competing."

— eMetropolitan.com, April 2026 St. Louis Market Report

One thing that doesn't get said enough in first-time buyer conversations: the offer framework above is market-dependent. If you're buying in St. Louis City with a 3.5-month supply, you can often submit an offer the day after you see a home and not lose it. You can ask for seller concessions toward closing costs without killing the deal. You can negotiate on inspection findings without the seller walking. The pressure is real in the suburbs — it's not uniform across the metro.

The buyers who consistently lose deals in hot markets share one trait: they're using a suburban strategy in a suburban market but operating on a city timeline. Speed in competitive pockets isn't optional. It's the product.

The Bigger Picture

Is the St. Louis Market Going to Crash? Here's the Honest Answer.

I get this question constantly, and I'd rather answer it directly than dance around it. The St. Louis housing market is not heading toward a crash. That's not optimism — that's what the data says.

The conditions that typically precede housing crashes — dramatic oversupply, speculative pricing disconnected from income fundamentals, widespread predatory lending — are not present in St. Louis right now. What we're seeing instead is a gradual normalization after the pandemic-era frenzy. Days on market are longer than they were in 2021 and 2022. Sellers have tempered expectations. Inventory is slowly rising.

The St. Louis market entered spring 2026 with homes selling at 95.5% of asking price metro-wide and 931 homes available in January — up from the inventory drought of recent years, but still not the kind of supply that pushes prices into freefall. The MSA median sold price of $285,000 represents a 3.64% year-over-year increase through April 2026. Steady. Not spectacular. Not collapsing.

What makes St. Louis particularly insulated from the kind of volatility you see in more speculative markets is structural: housing costs here run approximately 21.2% below the national average, and the overall cost of living is roughly 11% cheaper than the U.S. norm. People who move here from Chicago, Austin, or Nashville aren't buying for speculation — they're buying because the math makes sense for their lifestyle. That's a more durable demand base than markets that ran up 40% in 18 months on investor activity and remote-work migration alone.

For first-time buyers, the practical implication is this: if you find a home that fits your needs and your budget in 2026, you are not buying into a bubble. You are buying into one of the most affordable major metros in the country at a moment when the frenzied competition of 2021 and 2022 has cooled to a level that still favors sellers in the suburbs but gives you real room in the city. That's a window. It doesn't stay open forever.

The Bottom Line for 2026 Buyers

Know which submarket you're in and adjust your timeline accordingly. St. Charles County and hot pockets in St. Louis County require same-day decisiveness. St. Louis City gives you more time and more negotiating room.

Get genuinely pre-approved — not just pre-qualified — before you start touring homes. In competitive markets, pre-approval is table stakes, not a nice-to-have.

Look into MHDC's First Place Loan Program before you assume you need to save more. The cash assistance option may get you to the closing table faster than you think.

Don't try to time the market. Rates are where they are. Values are stable. The cost of waiting is the equity you're not building and the rent you're still paying.

Start With One Thing This Week

Pick one strategy from this list. Just one. Call five people in your sphere by Thursday. Pull this week's expired listings in your market and write two personalized notes. Or draft one piece of genuinely useful local market content for social. Don't try to implement all three simultaneously — you'll do none of them well. Do one, measure it, then add the next. That's how a pipeline gets built.