Managing Client Expectations in the 2026 Summer Market

Jul 08, 2026

Written by Discount Property Investor Team

The mid-summer real estate environment always brings its own unique set of challenges. By mid-July, we often see a specific type of client fatigue settling into the market. Buyers might be profoundly tired of losing out on homes or dealing with stubbornly high summer interest rates, while sellers might be growing impatient if their property didn't move during

the frenetic spring rush. As their agent, your job isn't just to open doors and schedule showings; it’s to expertly manage expectations and keep emotions grounded in reality.

In this comprehensive guide, we are diving deep into the psychology and data of the July 2026 housing market. Whether you are dealing with burnt-out first-time buyers or sellers holding out for unrealistic numbers, we will break down the strategies, scripts, and local market intelligence you need to navigate this season successfully.

1. Understanding the 2026 Summer Market Squeeze

To effectively guide your clients, you first need an airtight grasp of exactly what is causing their stress. The narrative of 2026 has been dominated by a tug-of-war between resilient buyer demand and a very slow drip of inventory relief, compounded by borrowing costs that refuse to drop significantly. For buyers, the primary roadblock is exhaustion. They have spent the better part of the spring touring properties, writing aggressive offers, and still coming up short. According to insights from David Lenoir's analysis of summer buyer fatigue, many buyers reach a breaking point by July. They become exhausted from touring dozens of homes and having their offers repeatedly rejected, which leads some to push back on incentives that were once standard, or even step away from the market entirely. However, the data also shows that summer consistently brings a wave of new listings—often up to 32% more fresh options than the autumn-to-winter slump. Educating buyers on this summer premium and seasonal inventory shift is crucial to keeping them motivated. On the financial side, we cannot ignore the elephant in the room: mortgage rates. As of July 2, 2026, the 30-year fixed-rate mortgage averaged 6.43%, according to Freddie Mac. While this is down slightly from the previous week, borrowing money to buy a home remains undeniably expensive compared to historical norms. Buyers are feeling the pinch in their monthly budgets, which makes them hypercritical of the properties they do view.

🏦 Interest Rates

Average 30-year fixed mortgage rate as of July 2026 (Freddie Mac).

🛑 Buyer Fatigue

Buyers are pushing back on waiving inspections and covering large appraisal gaps.

🏡 Seller Expectations

Sellers still expect spring-level bidding wars, so agents need clear, data-backed pricing conversations.

2. Drilling Down into the Data: The St. Louis Perspective

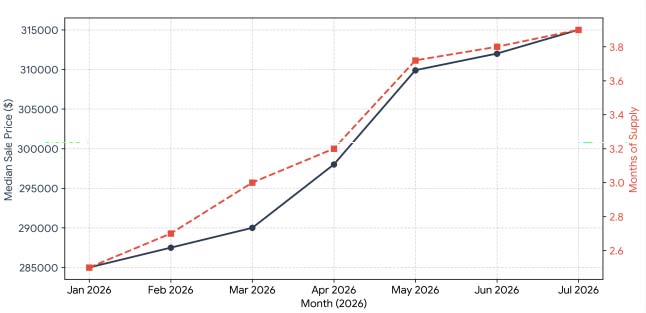

Real estate is hyper-local, and generic national headlines often do more harm than good when trying to calm an anxious client. If you are operating in our primary market, you must arm yourself with St. Louis-specific data to prove your points. Let's look at the numbers. The St. Louis housing market in mid-2026 is defined by its resilience and relative affordability, with housing costs in the region sitting approximately 39% below the national average. As of the latest reporting for the St. Louis MSA, the median sale price has climbed to roughly $309,900. While this is fantastic news for sellers regarding equity growth, it represents a very real hurdle for buyers stretching their budgets at a 6.43% interest rate. Furthermore, inventory dynamics vary wildly depending on exactly where your client is looking. Overall, the MSA holds about a 3.72-month supply of homes. However, if your buyers are hunting in St. Charles County, they are in one of the fiercest pockets in the region, with properties routinely going from list to under contract in just 7 days. Conversely, the City of St. Louis offers a slightly more nuanced environment with a median sale price closer to $235,000, giving buyers a bit more leverage to negotiate original prices and seller concessions.

St Louis Housing Market Trends (Jan - Jul 2026)

Source: Metropolitan Mortgage Corporation 2026 Data / MARIS Insights

3. For the New Realtor: Master the Art of Over- Communication

When a buyer loses a bid, or a seller’s home sits for two weeks without an offer, silence from their agent creates a vacuum. And in real estate, clients always fill a communication vacuum with anxiety and worst-case scenarios. If you are relatively new to the game and don't yet have decades of closed deals to rest your confidence on, you must make communication your absolute

superpower. Set a strict, non-negotiable schedule to update your clients twice a week. Tuesday mornings and Friday afternoons are generally the best touchpoints. Even if the update is simply, "No new activity today, but here is our strategy for the weekend open houses," you are showing that you are at the helm of the ship. Reassure them that summer markets have their own distinct rhythm. Families are on vacation, school preparation is beginning, and the buyer pool naturally thins out slightly compared to May. Script for the Fatigued Buyer: "I know missing out on Main Street was incredibly frustrating. But remember, the summer market traditionally brings a wave of new inventory as builders finish projects and delayed sellers finally list. According to current data, summer months can offer up to 32% more fresh options than the fall. We are in the best window of opportunity right now to find a property where the location and layout actually align for you."

For the Seasoned Realtor: Leverage Your Network and Creative Solutions

If you have a frustrated buyer who simply cannot find inventory in a highly competitive area like St. Charles County, it’s time to flex your veteran muscles. You cannot rely solely on the MLS. Lean heavily on the network you’ve meticulously built over the years. Call other top-producing agents in your market and ask directly about whisper listings or properties coming soon. Furthermore, when traditional financing at 6.43% is crushing your buyer's purchasing power, seasoned agents know how to pivot to creative solutions. This is the perfect time to explore

alternative financing structures. Owner financing, for instance, can be an incredible tool for the right property and the right seller, allowing buyers to bypass traditional lenders entirely while offering sellers a steady stream of income at a favorable negotiated rate. Similarly, connecting distressed sellers with fast-closing cash buyers can solve problems that traditional retail listings cannot touch. For your sellers, your network is equally important, but your most vital tool is the data. If a home isn't moving, you must have the tough, data-driven conversation about a price adjustment *now*, before the dog days of August hit and the market grinds to a pre-school-year halt.

Navigating the Seller Pricing Conversation

Managing seller expectations in July requires a delicate balance of empathy and hard facts. Many sellers are still operating under the assumption that their home will sell in 48 hours for $50,000 over asking, simply because their neighbor's house did in 2022. The 2026 market is seeking equilibrium. While the broader national market is finding balance, high interest rates mean buyers are strictly enforcing value. When presenting a price reduction, never frame it as a failure. Frame it as a strategic market repositioning. Show them the traffic data. If you have had 15 showings and zero offers, the market is universally rejecting the price, not the house. Use the local St. Louis data: with inventory stabilizing around a 3.72-month supply, "pricing right from day one" is the most critical factor to optimize returns. If they missed the mark on day one, a rapid correction is their best chance at avoiding a stale listing. Script for the Stagnant Seller: "We've had great foot traffic over the last 14 days, but the lack of paper offers tells us exactly what the market thinks. Buyers at a 6.43% interest rate are incredibly sensitive to pricing right now. To capture the attention of the fresh wave of buyers entering the market this weekend, we need to reposition the home at [New Price]. This puts us in a new search bracket and creates renewed urgency."

The Impact of Rising Costs on Specific Segments

It is also crucial to manage expectations regarding property types. Across various national markets, we are seeing a distinct divergence between single-family homes and attached dwellings (condos/ townhomes). Due to rising inflation, high HOA dues, and skyrocketing insurance premiums, the condo market is facing significant headwinds. If you are listing a condo this summer, prep your sellers for longer days on market and the potential need to offer buyer concessions to offset those high monthly carrying costs. The condo and townhome segment is struggling across many metros, reflecting cautious buyers amid economic uncertainty.

Coaching Takeaway: You Are the Pilot

Real estate transactions are inherently emotional. For most of your clients, this is the largest financial transaction of their lives, unfolding under the pressure of summer heat, ticking school-

district deadlines, and economic uncertainty. You are the pilot of this transaction. When there is turbulence—a low appraisal, a bad inspection report, or a sudden spike in rates—your clients will immediately look to you to see how they should react. If you panic, they panic. If you are calm, collected, and armed with actionable solutions, they will feel secure. Stay calm, stay communicative, and stay professional. Anticipate the roadblocks before they appear, communicate your strategies clearly, and remember that your ultimate value isn't in finding the house, but in guiding the human beings through the complex journey of buying it.