How Gen Z Is Changing Real Estate with AI in 2026

Jun 12, 2026

Written by Discount Property Investor Team

Walk into any coffee shop in a college town, and you'll likely find a Gen Z-er with three browser tabs open: one on Zillow, one running a ChatGPT thread about property tax rates in their target zip code, and one crunching numbers on a house-hacking calculator someone posted to TikTok. That is not an exaggeration. It's the 2026 homebuying reality for a generation that grew up with smartphones literally in hand — and it's already starting to reshape what the residential real estate industry looks like.

The numbers are still modest. According to the NAR's 2026 Home Buyers and Sellers Generational Trends Report, Gen Z accounts for just 4% of all primary-residence buyers. Baby Boomers still hold 42%. But that share will only grow, and the behavior patterns Gen Z brings with them are already forcing agents, lenders, and developers to rethink their entire playbook.

This isn't about Zoomers being tech-obsessed for its own sake. It's about a generation that watched housing prices spiral, saw their older siblings struggle with student debt and rent hikes, and made a calculated decision: if I'm ever going to own property, I need every data advantage I can find. They have weaponized information. And the real estate industry, frankly, is still playing catch-up.

The Gen Z home-buying tech stack

For older generations, the home search had a kind of ritual progression: drive the neighborhood, attend an open house, flip through a MLS packet the agent printed out. Gen Z skips most of that. Their journey is almost entirely digital until they're genuinely ready to make an offer — and even then, they've already done more due diligence than the average buyer of ten years ago had access to.

Phase 1: Discovery through AI-powered matching

The search doesn't begin with a city name and a price ceiling. It begins with a lifestyle query. Gen Z buyers use platforms that layer machine learning over traditional listing data, allowing them to filter by commute time to a specific employer, walkability scores to coffee shops or gyms, neighborhood noise levels pulled from environmental datasets, and even smart-home infrastructure compatibility. Plugging a vague wishlist into ChatGPT or Gemini to get neighborhood suggestions and hidden-cost breakdowns is now table stakes — not an edge case.

Realtor.com reported that 82% of Americans were already using AI for housing market research, with younger cohorts leading significantly. Gen Z isn't just Googling — they're having multi-turn conversations with AI assistants to model scenarios: "What would my all-in monthly cost be if I bought a $340,000 condo in this zip code, rented out one room, and claimed the mortgage interest deduction?"

Phase 2: The shortlist via VR and AR staging

Before a Gen Z buyer will spend 45 minutes driving to a showing, they want to have walked through the property three times on their laptop. 3D virtual tours are no longer a pandemic-era accommodation — they are a prerequisite. Any listing without one gets scrolled past.

What's newer is how this generation uses augmented reality staging. Rather than trying to mentally furnish a vacant space, they're dropping their own aesthetic into a floor plan digitally — testing a mid-century modern living room layout, checking whether a Murphy bed conversion would make the den functional, or mapping out where a home-office partition wall could go. They're not just touring a property. They're pre-renovating it, virtually, before committing to a showing.

This also connects to the house-hacking mindset that runs through Gen Z real estate culture. Many are evaluating properties not just as a place to live, but as an income-generating asset — and AR tools let them model that before they ever speak to an agent.

Phase 3: Automated financial pre-checks

The mortgage pre-approval process that once required weeks of paperwork and back-and-forth with a loan officer has been dramatically compressed. Algorithmic instant pre-approvals, automated asset and income verification, and digital-first lenders have cut underwriting timelines from days to minutes in many cases. For a generation with limited patience for friction, this matters enormously.

As Eric Hamilton of Rate noted, the technology now reaches across the entire loan lifecycle — not just origination. Monitoring, compliance checks, and post-close asset pulls are all increasingly automated. Gen Z buyers expect this. When a lender asks them to fax something, they experience something close to genuine confusion.

Sources: Harris Poll State of Real Estate 2026 (Stagwell); IPX1031 Homeownership Statistics 2026. Multiple responses permitted.

What Gen Z actually wants in a home

Growing up through the 2008 financial crisis, a global pandemic, and a decade of climate-anxiety news coverage has left a mark on what this generation values in property. They are not chasing the sprawling, four-bedroom suburban McMansion their parents dreamed about. Efficiency, future flexibility, and environmental footprint are the real drivers — and AI tools have made it practical to actually evaluate properties on those axes.

| Priority | What It Looks Like in Practice | How Tech Fits In |

|---|---|---|

|

Tech Integration |

Smart thermostats, automated security systems, and native high-speed internet infrastructure are viewed as baseline expectations rather than luxury upgrades. |

Gen Z buyers use listing filters, virtual tours, and AI-powered searches to identify smart-home features before ever visiting a property. |

|

Sustainability |

Solar panels, low-VOC materials, energy-efficient HVAC systems, and eco-friendly construction methods are highly valued. Nearly 70% of Gen Z buyers say they would exceed their budget for a greener home. |

Predictive AI tools estimate utility savings, maintenance costs, and ROI from energy-efficient upgrades, turning sustainability into a measurable financial benefit. |

|

Affordability Hacks |

Co-buying with friends, house-hacking through room rentals or ADUs, and purchasing in emerging neighborhoods instead of established markets. |

Rental income analyzers, cash-flow calculators, and AI-driven market tools help buyers model income potential before making an offer. |

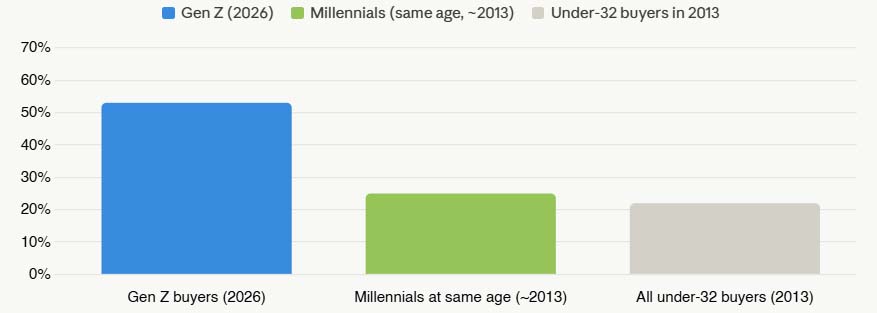

It's also worth noting what the NAR's 2026 data revealed about Gen Z's household composition at purchase: 53% of Gen Z buyers are purchasing alone — more than double the rate at which millennials were buying solo at the same age. That statistic says something significant about this generation's priorities. Many are actively delaying marriage and major life milestones specifically to get into the housing market sooner, treating homeownership as a prerequisite rather than a post-wedding milestone.

Solo homebuying rates by generation at comparable ages

Source: NAR 2026 Home Buyers and Sellers Generational Trends Report; NAR 2013 Generational Trends Report.

The trust paradox: high tech expectations, deep skepticism

Here is where it gets genuinely interesting — and where most real estate professionals misread the Gen Z buyer entirely.

The assumption is that because Gen Z uses technology for everything, they trust technology for everything. That is wrong. In fact, Cotality's AI in Housing 2026 Report — a landmark international study covering buyers across the U.S., Canada, the UK, and Australia — reveals something more complicated and more strategically important: Gen Z expects AI to be present, but they are among the most vocal about wanting human oversight of it.

What Cotality calls a "trust paradox" is really just a coherent position, once you understand how Gen Z thinks about information. They are digital natives who have also grown up watching misinformation spread at scale. They know that platforms optimize for engagement, not accuracy. They know that automated systems produce confident-sounding nonsense on a regular basis. They use AI aggressively as a research accelerant — not as an oracle.

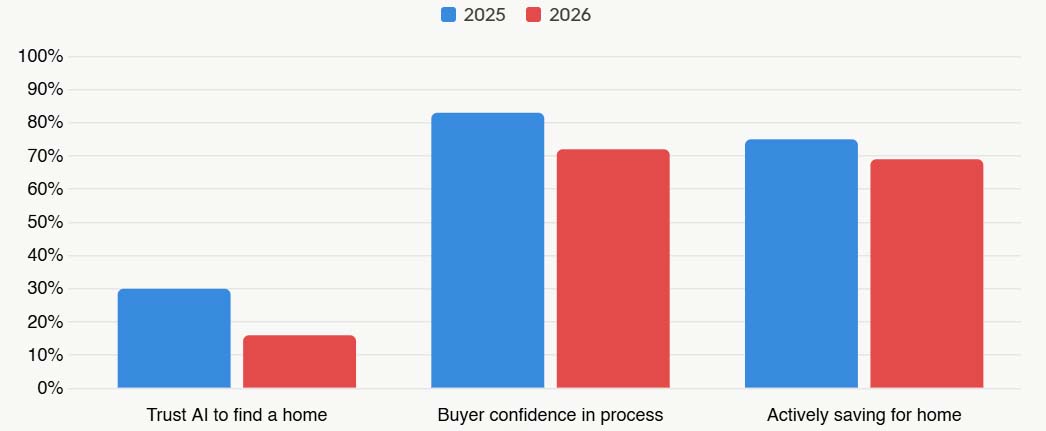

The tolerance for AI errors is remarkably low across all age groups, but it's important to understand the data correctly: only 22% of Gen Z say they are tolerant of AI mistakes in a real estate context. For context, that's actually higher than Gen X (11%) and Boomers (9%) — but it's still a floor, not a ceiling. These are buyers who will cross-check AI-provided property boundary data, who will question whether an automated valuation model is using stale comps, and who will lose trust in a platform permanently if they catch it displaying incorrect local tax information.

AI trust in homebuying: U.S. trend, 2025 vs 2026

Source: Cotality AI in Housing 2026 Report (April 2026). U.S. respondents only.

There's a practical implication hiding in those numbers. When 44% of buyers say they'd pay extra for human verification of AI outputs, that is not a sign of technophobia. That is a market signal. Buyers — especially younger ones — are telling the industry exactly what they're willing to pay for: accountability. The ability to say "a real human with local expertise double-checked this, and here's the paper trail."

Cotality's head of Data Science, Amy Gromowski, put it directly in the report's findings: "Buyers are not rejecting AI; they are asking for safeguards. They recognize AI's power to process massive datasets and speed up decisions. But when it comes to the largest financial transaction of their lives, accuracy and accountability are non-negotiable."

The solo buyer reality and what it means for agents

Return for a moment to that Fortune finding: 53% of Gen Z buyers are purchasing homes alone in 2026. That's a striking number, but the context matters. A 2025 Coldwell Banker survey found that 84% of Gen Z say they're actively delaying major life milestones — including marriage — to save for a home. This generation has reordered the traditional sequence of adult life events. Home first, partnership optional.

For agents and lenders, this reordering has concrete operational implications. The solo buyer doesn't have a co-borrower's income to lean on. They're often more conservative about stretching their budget, more analytical about cash-flow scenarios, and more likely to be researching every line item of a transaction before they come to the table. They show up having done real homework, and they will notice if an agent underestimates them.

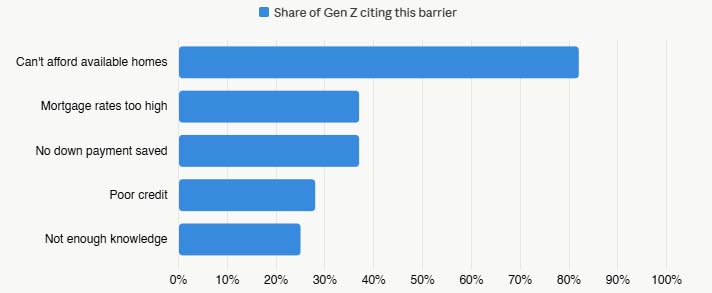

There's also the barrier reality to contend with, honestly. According to Harris Poll's State of Real Estate 2026, 37% of Gen Z cite both mortgage rate levels and lack of down payment savings as their primary homebuying barriers — and 25% say they simply don't have enough knowledge to pursue it. That knowledge gap is actually an opportunity. The Gen Z buyers who do push through to purchase are the ones who found trustworthy sources of information. Being that source — consistently, accurately, without a sales pitch layered over every response — is how professionals build long-term relationships with this cohort.

How local real estate professionals can actually adapt

The Gen Z opportunity isn't about adopting the flashiest tech. It's about understanding the specific trust architecture of this buyer and building your practice around it. They will find you through technology. But they will choose to work with you — and refer you — because of how you handled the moments where the technology fell short.

- Productize your local data knowledge. Don't just send a listing link. Send a one-page breakdown that maps out the neighborhood's actual walkability (not just the score — what the nearby amenities are), current municipal zoning rules relevant to ADU or room-rental legality, projected cash flow if they house-hack, and a clear property tax estimate. This is the layer of contextualized, verified information that AI platforms consistently get wrong or leave out — and Gen Z knows it.

- Lean into as-is transparency. If a home needs work, don't bury that. Use virtual remodeling tools to show buyers the financial upside and layout potential of a fixer-upper, explicitly. Gen Z is not scared of work if the numbers make sense — they're scared of being surprised. Show them the math upfront and they'll trust you more for it.

- Position yourself as the human verifier. Cotality's data is a gift to every agent who has wondered how to differentiate from Zillow. Forty-four percent of buyers want to pay for human verification of automated data. Build that into your value proposition explicitly: you are the person who checks the boundary survey, reviews the title recorder filings, catches the outdated tax data, and signs off on the accuracy of the automated valuation. That is not a soft skill. That is the product.

- Meet them where the research happens. Gen Z is not going to find you through a yard sign or a newspaper ad. They're on TikTok, YouTube, and Instagram consuming real estate education content. Short-form videos that explain property tax assessments, demystify title insurance, or walk through a house-hacking cash-flow model are not just marketing — they are the answer to that 25% knowledge gap Harris Poll identified. The agents building audiences on those platforms right now are planting seeds for the next five years of Gen Z buyer volume.

- Streamline your own process. If your onboarding still involves emailing PDFs back and forth for signatures, you will lose Gen Z buyers before the relationship starts. Digital document management, instant communication through text or chat, e-signature for everything — these are not differentiators for this demographic. They are the floor.

The bigger picture: a market in transition

The NAR's 2026 data shows first-time buyers at a record-low 21% of all purchases, with the median age of first-time buyers hitting 40 for the first time ever. The market is older, more equity-driven, and more structurally tilted toward existing homeowners than at almost any point in recent history. Gen Z's 4% share looks small in that context.

But NAR's own projections anticipate that as Gen Z approaches the historical median age of first-time buyers over the next decade, they will become an increasingly significant share of transaction volume. The professionals who build systems, relationships, and brand equity with this cohort now — before the cohort fully arrives — will be positioned well. The ones who wait until Gen Z buyers are 35% of the market to start learning their preferences will be rebuilding from scratch.

What makes this generation genuinely different isn't the apps they use. It's the mental model. Gen Z approaches real estate the way a financial analyst approaches a deal — with a spreadsheet, a stress test, and a healthy suspicion of anyone selling something. That combination of analytical rigor and human-trust deficit is not going away. It's going to define the market for the next 15 years.

The good news for professionals is that the trust paradox Cotality documented isn't a problem to solve. It's a market to serve. When buyers tell you in no uncertain terms that they will pay a premium for accountability and accuracy, they are telling you exactly what to sell. The challenge is having the discipline to deliver it consistently — and the credibility to make them believe you will.

The Gen Z homebuyer isn't looking to replace their real estate agent with an algorithm. They're looking for someone who can make the algorithm's outputs trustworthy. That's a fundamentally human job — and it's wide open.

If you're in that position — ready to own, financially capable of owning, but blocked by paperwork and scores — owner financing isn't your backup plan. For a lot of people, it's the only plan that actually gets you to the closing table.