Why Owner Financing is Winning the 2026 Housing Market

Jul 17, 2026

Written by Discount Property Investor Team

The Great Shift of 2026

When traditional bank lending tightens, creative financing naturally takes center stage. We are currently witnessing what housing economists have dubbed the "Great Housing Reset," a period marked by elevated institutional barriers, cooling price surges, and a renewed emphasis on deal structuring. For real estate newbies struggling to meet rigid loan requirements and seasonal investors looking to move properties quickly before the fall cooldown, owner financing has become one of the most powerful tools in the 2026 market. By bypassing institutional bureaucracy, it creates a direct, mutually beneficial agreement between buyer and seller.

The days of relying solely on generic 30-year fixed mortgages are fading. Buyers are tired of paying exorbitant origination fees, while sellers are looking for ways to maximize yield without leaving money on the table. Owner financing—also referred to as seller financing—shifts the paradigm. It allows individual property owners to act as the bank. Recent housing market predictions for 2026 highlight that as affordability gradually improves, alternative purchasing avenues will play a critical role in bringing sidelined buyers back into the fold.

What Exactly is Owner Financing?

Instead of a buyer seeking approval from a massive national lender, the seller themselves acts as the financial institution. The transaction is remarkably straightforward in theory, though it requires meticulous documentation in practice. The buyer makes a down payment directly to the seller and signs a promissory note detailing the interest rate, repayment schedule, and consequences of default. It is real estate at its absolute most entrepreneurial.

In this arrangement, the seller retains a security interest in the property (typically via a mortgage or deed of trust, depending on the state) until the final payment is made. This eliminates the need for strict underwriter scrutiny, W-2 verification hassles, and standard institutional red tape. As noted by industry experts examining how owner financing helps potential buyers make informed decisions, this flexibility allows capable individuals who might have unconventional income streams —like freelancers, entrepreneurs, or newly self-employed workers—to secure property.

“In today’s market, the best real estate deals are structured through terms—not found through listings.”

This reflects a growing reality in 2026: negotiation and flexibility are often more powerful than rigid institutional guidelines.

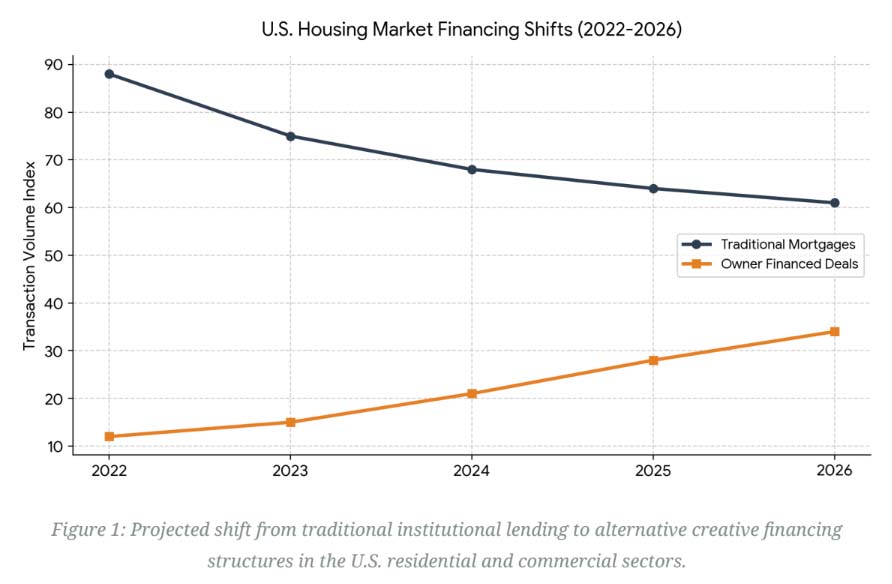

The Data: Financing Trends in 2026

Why the sudden surge in alternative arrangements? Look at the numbers. While national average mortgage rates have somewhat stabilized below the extreme peaks of recent years (comfortably avoiding the dreaded 7% and 8% marks), they are still substantially higher than the historically anomalous sub-3% era. This environment creates friction. Buyers cannot afford the monthly payments at traditional rates, and sellers refuse to drop their asking prices.

The gap is bridged through terms. Sellers are willing to offer a slightly below-market interest rate to the buyer to maintain their high purchase price. The buyer gets the house without jumping through hoops, and the seller turns their illiquid asset into a performing note that generates monthly cash flow.

A Win-Win Strategy: Breaking Down the Benefits

The beauty of this framework lies in its mutual utility. Let's analyze exactly how both sides of the transaction come out ahead.

| Benefit Category | For the Buyer (Newbie) | For the Seller (Investor) |

|---|---|---|

|

Speed of Execution |

Close in days instead of weeks. Avoid 45-day waits for bank underwriting and appraisal contingencies. |

Liquidate inventory quickly and sell before seasonal slowdowns affect the market. |

|

Qualification Standards |

Bypass rigid bank guidelines and focus on your actual ability to pay instead of relying solely on FICO scores. |

Set your own buyer requirements by evaluating character, local ties, and down payment strength. |

|

Cost Mitigation |

Avoid costly bank origination fees, private mortgage insurance (PMI), and unnecessary lender charges. |

Generate monthly interest income, increasing your property's overall return on investment. |

|

Flexibility |

Negotiate customized terms such as interest-only payments or balloon payments based on future income. |

Spread capital gains over multiple years through installment-sale tax advantages. |

How to Leverage Owner Financing Today

For the Aspiring Buyer (Newbies)

Use this strategy to secure your first property without needing a flawless credit profile or a massive institutional loan. The key is finding the right seller. You aren't going to find these deals by blindly submitting offers on the MLS to sellers who need cash to buy their next home. Instead, look for sellers who own their properties "free and clear" (without an existing mortgage). These are often older landlords tired of maintenance, inherited property owners, or seasoned investors looking to transition to passive income.

When approaching these sellers, focus on their pain points. Are they tired of property management? Do they want a steady, reliable income without the headache of tenants calling about a broken toilet at 2 AM? Pitching owner financing correctly requires showing the seller that they are upgrading from a "landlord" to a "lender." You can learn more about framing these conversations and understanding the process of acquiring real estate without relying on conventional bank loans.

For the Seasoned Real Estate Investor

If you are offloading a flip, managing a portfolio of single-family homes, or transitioning out of a summer rental property, offering seller terms can drastically expand your buyer pool. Consider a local market scenario, such as neighborhoods in St. Louis, Missouri. If you have a solid, well-rehabbed brick home but local retail buyers are getting spooked by bank rates, advertising "Seller Financing Available" will flood your inbox with applicants. You can often command a higher purchase price(because you are offering a premium service: the loan itself) and turn a stagnant property into a performing, interest-bearing asset.

Legal Realities and Important Caveats

While the benefits are profound, it is vital to acknowledge that we are operating in a highly regulated environment. This is not the Wild West of real estate. As noted by recent consumer protection updates, federal Truth in Lending Act protections apply to many of these transactions. Understanding why seller financing is completely legal and becoming more popular is crucial, but it must be done by the book.

Never rely on a napkin contract. Both parties should utilize qualified real estate attorneys to draft the Promissory Note and the Mortgage or Deed of Trust. Furthermore, using a third-party loan servicing company is highly recommended. These companies collect the buyer's monthly payment, handle escrow for taxes and insurance, provide end-of-year tax forms, and distribute the remaining funds to the seller. This removes the emotional component and professionalizes the arrangement,ensuring everyone stays compliant and protected.

It's also important to be aware of "due-on-sale" clauses if the seller has an underlying mortgage. Strategies like "Subject-To" financing or wraparound mortgages exist to navigate this, but they carry distinct risks if the original lender discovers the transfer and demands full repayment. Transparency and proper legal counsel are your best defense.

Advanced Strategies: Pushing the Envelope in 2026

The fundamental premise of owner financing opens the door to more advanced creative strategies. For example, investors are increasingly utilizing "Lease Options" (Rent-to-Own) as a stepping stone. In this model, the buyer pays a non-refundable option fee for the right to purchase the property at a fixed price within a specified timeframe (e.g., three years). A portion of their monthly rent may be credited toward the eventual down payment. This gives the buyer time to repair their credit or build job history, while the seller secures a highly motivated tenant who treats the property like their own.

Another powerful tactic is the "Subject-To" deal. Here, the buyer takes over the payments of the seller's existing mortgage, while the deed is transferred to the buyer's name. In the 2026 landscape, where many properties still hold underlying mortgages secured during the low-rate environments of 2020 and 2021, acquiring a property "subject to" a 3% or 4% mortgage is essentially striking gold. It requires careful negotiation and a deep understanding of how to buy real estate using creative financing safely.

Market Nuances: St. Louis and the Midwest Focus

While national trends dictate the macro-environment, local dynamics are where fortunes are made. The midwestern housing market, specifically St. Louis and its surrounding metropolitan area, presents a unique incubator for creative financing. The region boasts a diverse housing stock, ranging from historic brick multi-families to sprawling suburban single-family homes. Because price points in these markets are generally more accessible than coastal extremes, the barrier to entry for owner- financed down payments is much lower.

For an investor operating in Missouri, a 10% or 15% down payment on a $250,000 property is vastly more achievable for a retail buyer than the same percentage on a $800,000 property in California. This demographic reality means that real estate operators who master owner financing locally can build massive, performing note portfolios very quickly. They aren't just selling houses; they are creating long-term wealth through localized, decentralized banking.

The Bottom Line

In a market where agility wins, owner financing allows you to write your own rules and close deals that traditional banks would leave on the table. We are moving further away from the days when a central bank's decisions dictated the fate of every single real estate transaction. By understanding the mechanics of seller financing, protecting yourself legally, and targeting the right demographics, you are no longer at the mercy of the market. You are making the market.

As 2026 progresses, expect to see the operators who embrace creative capital pull significantly ahead of those waiting for traditional lending to return to an era that has long since passed. The shift is already happening—make sure you're positioned to capitalize on it.