How Much House Can Gen Z Afford in the U.S. in 2026? Expert Guide

Mar 27, 2026

Written by David Dodge

Key Insight:

A typical Gen Z buyer now needs an estimated income of around $111,000 annually to comfortably afford a median-priced home in the United States—far above the national median income.

Homeownership in the United States has historically been associated with long-term wealth building, stability, and upward mobility. However, for Generation Z—those entering adulthood in a post-pandemic, high-inflation economy—the pathway to owning a home has become increasingly difficult. Rising home prices, elevated borrowing costs, and slower wage growth have collectively reshaped affordability in ways not seen in decades.

Recent data suggests that nearly two-thirds of Gen Z Americans are struggling to meet housing costs, underscoring a structural imbalance between earnings and real estate prices (Redfin Research). This report examines the central question facing millions of young adults today: how much house can Gen Z realistically afford in the current U.S. market?

Defining Housing Affordability in 2026

Affordability is not simply about the listing price of a home; it is fundamentally tied to income, debt obligations, and borrowing costs. Financial institutions continue to rely on the widely accepted “28/36 rule,” which recommends that no more than 28 percent of gross monthly income be allocated toward housing expenses, while total debt obligations should not exceed 36 percent.

These benchmarks are still used by lenders and are supported by research from the National Association of Home Builders. However, in today’s market, adhering strictly to these guidelines often results in a purchasing power that falls significantly below the median home price.

In practical terms, this means that affordability is increasingly constrained not by financial discipline alone, but by structural market forces that limit access to entry-level housing.

The Income Gap Driving Gen Z Affordability Challenges

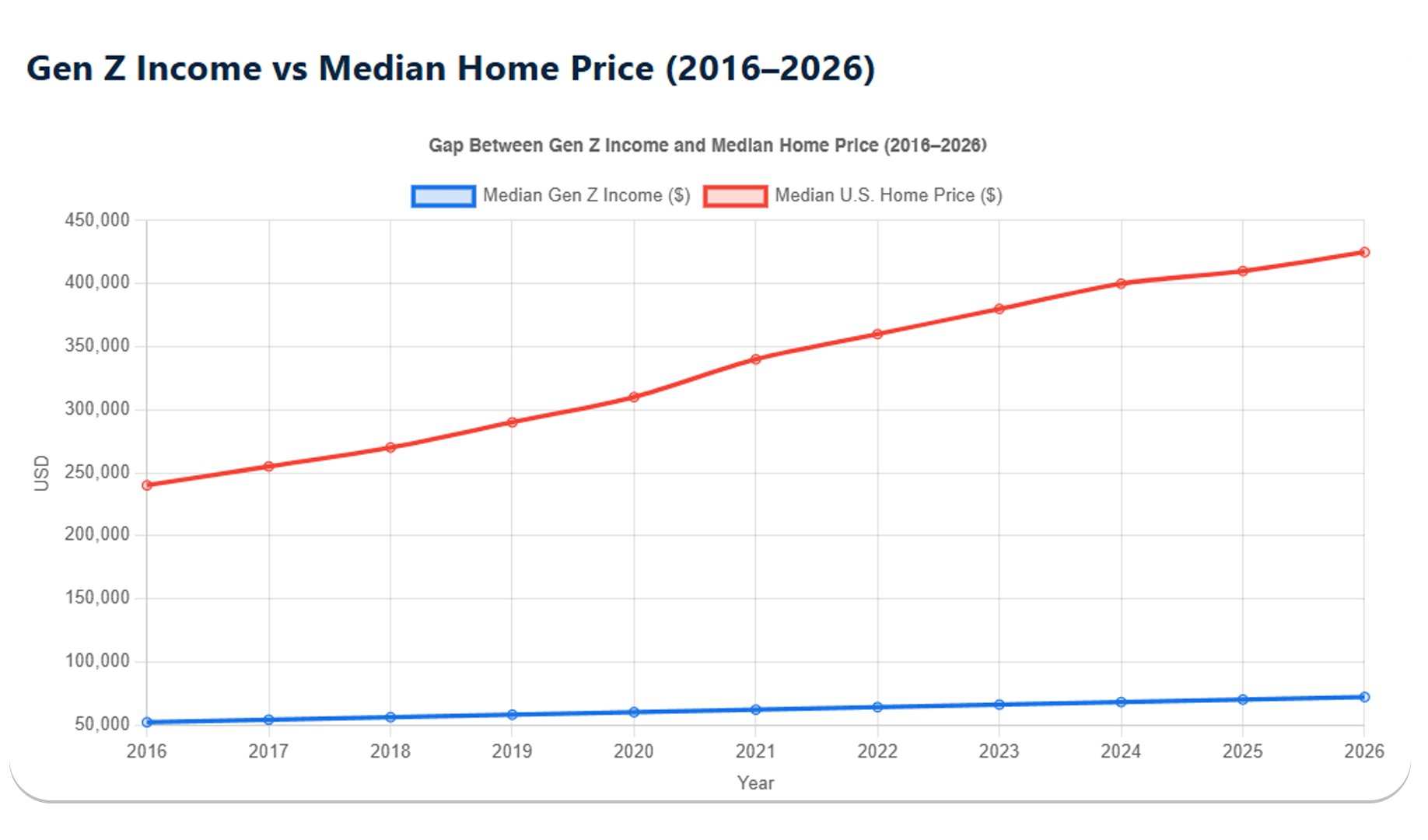

One of the most critical factors shaping Gen Z’s homebuying potential is the widening gap between income and home prices. Over the past several years, home values have risen at a pace that has far outstripped wage growth, creating a disconnect that disproportionately affects younger buyers.

Estimates indicate that an annual income of approximately $111,000 is required to afford a median-priced home under current mortgage conditions (Redfin Press Data). This figure stands in stark contrast to the national median household income, which remains significantly lower. For many Gen Z individuals early in their careers, reaching this income level is not immediately feasible.

As a result, affordability is not simply a budgeting issue—it is a systemic challenge that reflects broader economic conditions.

Monthly Cost Reality and True Ownership Expenses

Understanding what a buyer can afford requires looking beyond the headline price of a home. Monthly housing costs include mortgage payments, property taxes, homeowners' insurance, and ongoing maintenance expenses. Together, these components determine the actual financial burden of homeownership.

Financial experts emphasize the importance of maintaining a sustainable debt-to-income ratio, generally below 36 percent. However, many buyers—particularly in high-cost markets—are exceeding this threshold to enter the housing market (Wall Street Journal Guide).

For Gen Z, this often means making trade-offs, such as purchasing smaller homes, accepting longer commute times, or delaying homeownership altogether.

A Realistic Affordability Scenario

To illustrate the financial constraints facing Gen Z, consider a hypothetical buyer earning $60,000 annually. Based on standard affordability guidelines, this individual could allocate roughly $1,400 per month toward housing costs. Depending on interest rates and other variables, this translates to a home price range of approximately $200,000 to $250,000.

This range falls well below the current median home price in the United States, highlighting the gap between what young buyers can afford and what is available in the market.

Income vs. Home Price Gap

Geographic Variability and Strategic Relocation

Location plays a decisive role in determining affordability. While coastal cities and major metropolitan areas remain largely out of reach for many Gen Z buyers, more affordable opportunities exist in secondary and tertiary markets.

Data indicates that Gen Z buyers are increasingly targeting regions in the Midwest and the South, where median home prices are lower, and inventory is more accessible (RealEstateNews Analysis). This shift represents a broader migration pattern driven by affordability constraints rather than lifestyle preference alone.

Structural Barriers Unique to Gen Z

Compared to previous generations, Gen Z faces a combination of financial and economic challenges that compound affordability issues. Many entered the workforce during or after the COVID-19 pandemic, a period marked by economic uncertainty and rising living costs. At the same time, student loan obligations and high rental expenses have limited their ability to save for down payments.

Additionally, the U.S. housing market continues to experience a significant supply shortage, particularly in entry-level housing. This shortage places upward pressure on prices and intensifies competition among buyers.

These factors collectively create an environment in which affordability is constrained not just by individual finances, but by systemic limitations in housing availability.

Changing Perspectives on Homeownership

In response to these challenges, many Gen Z individuals are re-evaluating traditional assumptions about homeownership. Rather than viewing it as an immediate milestone, they are increasingly prioritizing financial flexibility, debt reduction, and alternative investments.

This shift reflects a broader cultural change in how younger generations approach wealth building. While homeownership remains a long-term goal for many, it is no longer seen as the only pathway to financial security.

Emerging Strategies for Entering the Market

Despite the obstacles, some Gen Z buyers are finding ways to navigate the housing market through creative strategies. These approaches often involve rethinking traditional buying models and leveraging alternative financial structures.

Common approaches include purchasing homes with the intention of renting out portions of the property, partnering with friends or family members to share costs, and relocating to more affordable markets. Others are utilizing government-backed loan programs that allow for lower down payments, reducing the initial barrier to entry.

These strategies highlight a growing trend toward adaptability and innovation among younger buyers.

Implications for the Housing Market

The affordability challenges facing Gen Z are not only a concern for individual buyers—they also have broader implications for the real estate market. As younger generations delay homeownership, demand for rental housing continues to rise, contributing to increased rental prices.

At the same time, there is a growing demand for smaller, more affordable homes, particularly in emerging markets. This shift presents opportunities for developers and investors to focus on entry-level housing and alternative ownership models.

Understanding these trends is essential for stakeholders seeking to navigate the evolving housing landscape.

Outlook for the Future

Looking ahead, several factors will influence whether affordability improves for Gen Z buyers. Interest rate trends will play a critical role, as lower borrowing costs can significantly increase purchasing power. Similarly, efforts to increase housing supply—particularly in the entry-level segment—could help alleviate price pressures.

Wage growth and policy interventions may also contribute to improving affordability, although meaningful change is likely to take time.

In the near term, however, affordability challenges are expected to persist, requiring continued adaptation from both buyers and industry participants.

Conclusion

The question of how much house Gen Z can afford does not have a single answer. It varies based on income, location, and financial strategy. However, the broader conclusion is clear: for most Gen Z buyers, affordability falls below the median home price in the United States.

Navigating this environment requires a combination of financial discipline, strategic decision-making, and flexibility. While homeownership remains achievable, it increasingly demands a level of planning and adaptability that sets this generation apart from those that came before.

Bottom Line:

Gen Z affordability is defined not just by income, but by strategy, market conditions, and the ability to adapt in one of the most challenging housing environments in modern U.S. history.