Top 5 Owner Financing Companies in St. Louis (2026)

Jun 11, 2026

Written by Discount Property Investor Team

Rising interest rates and rigid underwriting have pushed thousands of St. Louis families out of traditional mortgage eligibility. Here's what real, local owner-financing actually looks like — who's doing it, how it works, and why it may be the most honest path to homeownership left in 2026.

Let me be straight with you about something nobody in the real estate industry wants to say out loud: the traditional mortgage market in 2026 was not designed for most working people. It was designed for W-2 employees with two years of clean tax returns, a credit score above 680, and enough savings to cover both a down payment and six months of reserves. If that doesn't describe you, you already know the feeling — the pile of documents, the underwriter conditions, the denial letter that arrives with no real explanation.

I've watched this play out across St. Louis for years. A family makes decent money running a small business or doing contract work. They've been paying $1,400 a month in rent without a single late payment for four years. They have money saved. And a bank still tells them no because their 1099 income looks "irregular" on paper. It's genuinely maddening.

That's why owner financing — sometimes called seller financing — has moved from a niche workaround to a real, structured path for a growing number of St. Louis buyers. And in 2026, it's more organized, more transparent, and more legally sound than it's ever been.

June 2026

home price in 2026

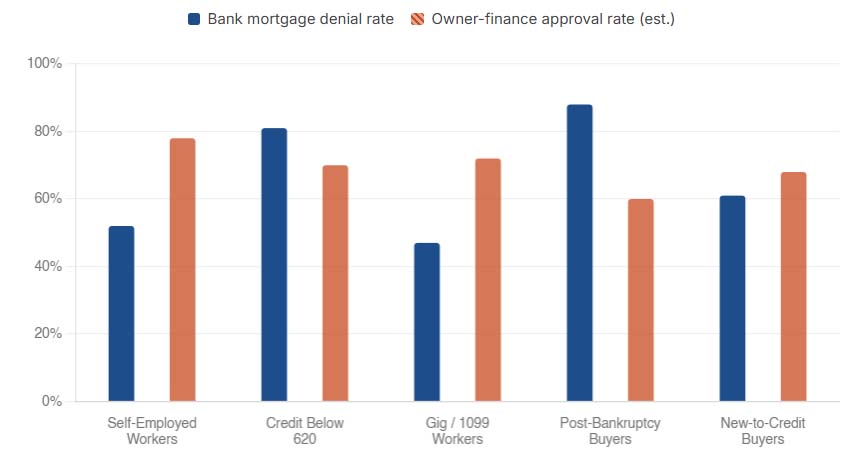

Mortgage Denial Rates by Applicant Type — St. Louis Metro Area

Comparing traditional bank denial rates vs. owner-financed approval rates across common buyer profiles, 2024–2025

Sources: CFPB Home Mortgage Disclosure Act (HMDA) data 2025; Urban Institute Housing Finance

Policy Center estimates, Missouri REALTORS® market data 2025.

Why Traditional Mortgages Are Harder Than Ever in St. Louis

The Federal Reserve's rate cycle changed the math permanently for a lot of buyers. When rates were at 3%, a borderline application could still pencil out. At today's rate environment hovering above 7%, the monthly payment on a $200,000 home is nearly $400 more per month than it was three years ago. That squeezes more buyers below the debt-to-income thresholds banks require, even when those buyers are financially responsible people who pay their bills on time.

But rates are only part of the story. The real wall for St. Louis buyers is documentation. The city has a large and growing population of self-employed contractors, small business owners, gig-economy workers, and entrepreneurs — people whose income is real but whose tax returns look complicated. A standard Fannie Mae-backed loan requires two years of self-employment tax returns, a year-to-date profit and loss statement, and often a CPA letter. Miss one piece, or show one bad year in 2022 when business was slow, and you're out regardless of what you make today.

According to CFPB's Home Mortgage Disclosure Act data, denial rates for self-employed applicants nationally ran significantly higher than for W-2 borrowers throughout 2024 and 2025, with credit-related denials and insufficient documentation accounting for the majority of rejections in mid-range price markets like St. Louis.

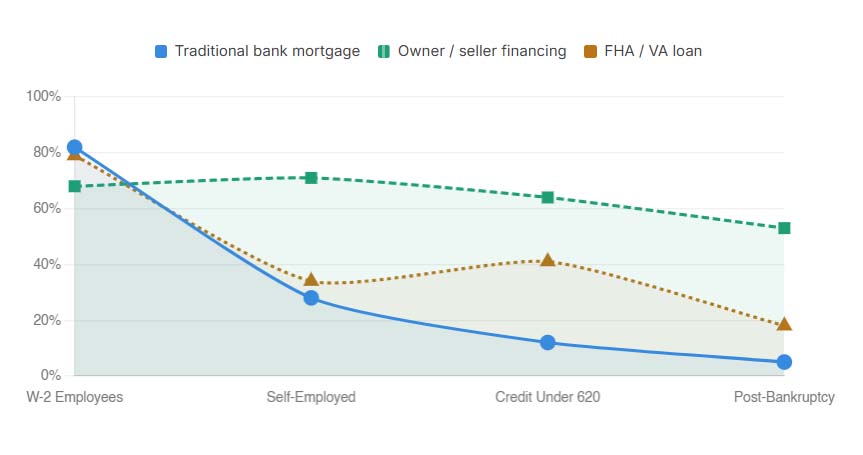

Homeownership Gap: Traditional vs. Alternative Financing Pathways

Share of prospective buyers who successfully closed on a home within 12 months, by financing path attempted (2024–2025, Missouri)

Sources: Urban Institute Housing Finance Policy Center, 2025 report; Missouri Housing Development Commission annual report; CFPB HMDA data.

What Owner Financing Actually Is — and Isn't

Owner financing gets tangled up with terms like "rent-to-own," "lease-purchase," and "contract for deed" in a way that confuses a lot of buyers. Let me lay this out plainly.

In a true owner-financed transaction, the seller of the property acts as the lender. You agree on a purchase price. You put money down. The seller holds a promissory note — a legal document stating that you owe them the remaining balance — and a deed of trust or contract for deed secures the property as collateral. You make monthly payments directly to the seller. No bank involved. No 90-day underwriting process. No loan officer who disappears for two weeks and then sends you a list of 14 conditions.

This is fundamentally different from a lease-purchase, where you're renting with an option to buy later but don't actually own anything yet. With proper owner financing — especially through a recorded deed of trust — your ownership interest is established from closing. The Missouri Revised Statutes, specifically Chapter 443, governs how these instruments are written, recorded, and enforced. When done correctly with a licensed real estate attorney, you have real, enforceable title rights.

The key distinction that makes owner financing work in the St. Louis context is this: the companies doing it well own their properties outright. No bank lien on the property means no bank approval required for you to buy it. The seller can set their own terms because they're the only party whose agreement matters.

The Top 5 Owner-Financing Sources in St. Louis Right Now

Not all owner-financing opportunities are created equal. Some are individual landlords selling a single property who have no idea what they're doing legally. Others are professionally managed investment firms that have structured hundreds of these deals and have their documentation tight. For buyers, the difference matters enormously — a poorly structured deal can leave you in legal limbo if the seller has an undisclosed lien or the paperwork isn't properly recorded.

Here are the legitimate, professional sources operating in the St. Louis metro area in 2026:

Greater St. Louis Metro · Eastern MO

1. House Sold Easily

One of the most established local real estate investment firms in the area, House Sold Easy maintains a rotating inventory of fully rehabilitated homes specifically reserved for buyers seeking alternative financing. Their approval process centers on two things: current income stability and down payment, not credit scores or tax return history. Closings typically happen within two weeks, and all transactions are recorded with the St. Louis County Recorder of Deeds. They own their properties free and clear, which means no outside lender can interrupt the deal.

St. Louis Area Suburbs · Bank-Free

2. Wealth Bridge (Wealth Bridge Owner Finance)

Nearly 20 years in the alternative financing market make Wealth Bridge one of the most experienced operators locally. Their model is explicitly built for buyers with damaged or nonexistent credit, with underwriting that focuses entirely on household budget capacity. What separates them from most is the face-to-face, relationship-driven approach to structuring terms. They sit down with buyers, work through what's actually affordable, and build a payment structure from the ground up — without any bank friction. Their stated goal is transitioning buyers out of the rent cycle into equity-building ownership.

STL City, St. Charles & St. Louis County

3. FasterFunds Lending Network

FasterFunds is primarily known as a hard-money lender for rehabbers and landlords, but their deep integration into the local investment ecosystem makes them a significant engine for owner-financed properties. Through their network of "buy-and-hold" investors across St. Louis City, St. Louis County, and St. Charles County, they regularly facilitate owner-financed notes or contract-for-deed arrangements when an investor wants to exit a property while keeping the cash flow by acting as the bank for a local family. Asset and equity-driven underwriting means the property itself matters more than your FICO.

St. Charles, Lincoln & Warren Counties

4. Local Broker-Investor Arms (e.g., Meyer & Company Real Estate)

Several boutique real estate brokerages across the St. Louis metro operate proprietary investment arms that carry "broker-owned" inventory. These licensed professionals understand Missouri real estate compliance deeply and can write legally sound lease-purchase agreements or contracts for deed that protect the buyer's equitable title from day one. Because they're licensed, they're also accountable to the Missouri Real Estate Commission — an added layer of consumer protection you don't always get with individual investors. This source is particularly well-represented in the outer-ring counties west of St. Louis City.

South City, Florissant & North County

5. Regional Independent Portfolio Operators

The final tier consists of private asset management groups holding between 20 and 50 residential units across areas like South City, Florissant, and independent municipalities in North County. These firms prioritize housing stabilization over churn — they actively prefer transitioning move-in-ready brick homes into owner-finance arrangements because a buyer-occupant takes better care of the property than a renter. Terms are relationship-driven and negotiated face-to-face directly. The inventory here tends to be classic St. Louis brick construction, which holds value well over time.

Head-to-Head: How These Sources Compare

|

Company / Source |

Best For |

Underwriting Focus |

Typical Timeline |

|---|---|---|---|

|

House Sold Easily |

Turnkey updated homes; fast closings |

Income & down payment |

2 weeks |

|

Wealth Bridge |

Severe credit issues; equity building |

Household budget review |

2–3 weeks |

|

FasterFunds Network |

Investor-rehabbed properties |

Asset & equity driven |

2–4 weeks |

|

Broker-Investor Arms |

Legal compliance, outer counties |

Income + moderate credit |

3–5 weeks |

|

Portfolio Operators |

Historic brick homes; North County properties |

Relationship & trust-based |

Varies |

What the Approval Process Actually Looks Like

One of the biggest misconceptions about owner financing is that it's a handshake deal with no real process. The legitimate operators in St. Louis don't work that way. Here's what a real intake process typically looks like with a company like House Sold Easy or Wealth Bridge:

Step 1: Income verification

You'll provide recent bank statements — usually two to three months — showing consistent deposits that align with your stated income. This replaces the two-year tax return requirement that kills most bank applications for self-employed buyers. What the seller wants to see is simple: can you make this payment every month based on what's actually hitting your bank account right now?

Step 2: Down payment confirmation

Owner-financed deals in St. Louis typically require a down payment ranging from 5% to 15% of the purchase price, depending on the seller's terms and the buyer's credit profile. This is the seller's primary hedge against default risk. The stronger your down payment, the better the terms you'll generally receive — lower interest rate, longer amortization, more flexibility on the monthly payment structure.

Step 3: Property selection and terms negotiation

Unlike a bank loan, where you find the house first, and the bank underwrites it second, with owner financing, the inventory and the financing are bundled together. You choose from the seller's available properties and negotiate the terms simultaneously. Interest rates on owner-financed deals in Missouri typically run between 8% and 12% — higher than conventional rates, but the trade-off is real: you're getting a house and building equity rather than paying rent indefinitely.

Step 4: Closing and recording

This is where working with professional operators matters most. A legitimate deal closes with a title search, a promissory note, and a properly recorded deed of trust or warranty deed filed with the appropriate recorder's office — either the St. Louis County Recorder of Deeds in Clayton or the St. Louis City Recorder downtown. Recording protects your ownership interest under Missouri law. Any seller who wants to skip this step is a seller you should walk away from.

Under Missouri Revised Statutes Chapter 443, owner-financed transactions are typically secured through a combination of a Promissory Note and a Deed of Trust (or, less commonly, a Contract for Deed). The recorded deed establishes legal ownership and is filed with the county recorder's office where the property is located. Missouri law recognizes these instruments as legally binding purchase agreements. Buyers should insist on a recorded deed and work with a licensed Missouri real estate attorney at closing to review all documents before signing.

The Real Financial Math: Is It Worth It?

Let's talk numbers honestly, because owner financing gets criticized — sometimes fairly — for carrying higher interest rates than conventional loans. If you can get a conventional mortgage at 7.1% and an owner-financed deal is offered at 10%, that's a real cost difference. On a $175,000 home, that gap is roughly $270 more per month. Over five years, that's about $16,000 in additional interest.

But here's the counterpoint that rarely gets included in that comparison: what are you paying right now in rent? If you're in a St. Louis apartment or rental house at $1,300 to $1,500 a month, none of that money is building equity. Over five years, that's $78,000 to $90,000 paid to a landlord with zero return. Even at a 10% owner-finance rate, every payment you make is partially reducing principal and building ownership in an asset that appreciates over time.

The Urban Institute's Housing Finance Policy Center has consistently documented in its research that homeownership — even when achieved through non-traditional financing — generates significantly more long-term wealth than renting for families in mid-range housing markets like St. Louis. The equity gap between owners and renters compounds dramatically over a decade, regardless of how the initial purchase was financed.

The smarter framing isn't "is 10% too high?" — it's "what is the cost of waiting another three years trying to qualify for a conventional mortgage that may never happen?" For a lot of St. Louis families, the answer to that question makes owner financing the obvious financial choice even before accounting for the emotional and stability benefits of owning your own home.

What to Watch Out For

I'd be doing you a disservice if I only talked about the upside. Owner financing, when done badly, can be a mess. Here's what separates a legitimate deal from one you should avoid:

The deed must be recorded

If a seller tells you they'll record the deed "after a few payments" or "once you prove you're serious," walk away. Recording is not a favor — it's the legal step that makes your ownership real. An unrecorded interest can be wiped out by other creditors or claims against the seller. Insist on recording at closing, period.

Title search is not optional

Before you close on any owner-financed property, a title search must be conducted to verify the seller actually owns the property free and clear and that there are no outstanding liens, judgments, or encumbrances. Professional operators do this automatically. Anyone who resists a title search is concealing something.

Read the balloon payment terms carefully

Some owner-financed deals are structured with a balloon payment — meaning after a set period (often 3 to 7 years), the remaining balance becomes due in full. The assumption is that you'll have improved your credit and refinanced into a conventional mortgage by then. That's a reasonable structure, but you need to understand exactly when the balloon hits and what your refinancing plan is. Don't sign a balloon note without a clear plan for what happens at maturity.

Work with a Missouri real estate attorney

Attorney fees at closing are not something to skip on to save a few hundred dollars. A licensed Missouri real estate attorney will review your promissory note, your deed of trust, and all closing documents before you sign anything. The cost — typically $400 to $800 in St. Louis — is money extremely well spent.

The Bigger Picture: Who Owner Financing Serves in 2026

The narrative around owner financing has shifted noticeably over the past few years. It used to be positioned almost apologetically — as the option for people who "couldn't qualify" for a real mortgage. That framing was always a little condescending, and it's increasingly inaccurate.

Owner financing in St. Louis today serves a wide range of buyers who are financially capable but structurally excluded from the conventional system. That includes long-term self-employed business owners, immigrants, and first-generation Americans building credit history for the first time, people who went through a medical bankruptcy or divorce that left a crater in their credit score but who have completely rebuilt their financial lives, and younger buyers who have high income but a thin credit file because they've been responsible about avoiding debt.

None of these people is a financial risk in any meaningful sense. They are excluded by a system that uses proxies — credit scores, tax return formats, debt ratios — that don't actually measure what they claim to measure for everyone. Owner financing cuts through those proxies and gets back to the fundamental question: Can you make this payment every month? The answer, for a lot of St. Louis families, is clearly yes.

As CFPB data continues to document growing disparities in mortgage access by income type and credit profile, the role of professionally structured owner financing in local housing markets will only grow. The companies doing it right in St. Louis — the ones recording deeds, conducting title searches, and building transparent payment structures — are providing a genuine service that the conventional mortgage market has decided it doesn't want to offer.